The Next Crash is Looming; A Soft Landing is Unlikely

Depressing thoughts following a NIESR Seminar

Many fish and chip portions could have been wrapped in the reams were written about the UK’s recent budget. For the short, electronic version I recommend this insight from Ewen Stewart. Short version, Mr Hunt and his ship of fools are reshuffling the deckchairs on the Titanic – the Titanic being the UK economy, not the dead men walking of the Tory party. Tragically for the UK and its residents, Starmer’s policies are to all intents and purposes the same.

That won’t make much difference in the medium term if a recent discussion at the National Institute for Economic and Social Research, is correct. NIESR is a fine not-for-profit which therefore relies on being academically correct , (or as close to correct as any macro-economist can be), rather than subscribing to political dogma. The topic was Assessing Cycles and Structural Changes in Markets and it was grim. The speakers were Andrew Smithers (ex-Warburg) and Peter Oppenheimer (Goldman Sachs). Smithers painted and justified a worrying macroeconomic picture, Oppenheimer found some rays of hope.

The short version was that the US equity market is overvalued, overdue a correction and will come down soon. When the S&P 500 falls every other index will follow, under the “America sneezes and the rest of the world catches a cold” rule. Whether that is a soft landing or a hard one (i.e. a crash) depends on three things.

To ameliorate the crash’s impact central banks could keep printing money, known variously as informal borrowing, kicking the can down the road or the magic money tree. As we have seen since the global financial crisis, this leads inexorable to inflation and higher interest rates.

It’s only recently that real interest rates (that is interest minus inflation) have been positive. Foe several years borrowers (mostly governments and some blue chips) have been paid to borrow. This has had multiple impacts. If debt is free few companies will raise money through equity, so the cheap debt has done stock markets no good. That in turn has undermined performance of investors – be they pension funds or households in search of a return – and turbocharged the profits of (debt heavy) private equity model. Indeed the Norwegian Sovereign Wealth Fund has been seeking permission to invest in private equity. The past decade has been poor for wealth creation for most investors. The Bank of England Pension Fund’s derivatives problem of the Truss bond market hiatus was in part a symptom of the struggle investors have had to find a return. Cheap money is no panacea and it can’t last for ever.

Oppenheimer outlined two hopes for a soft landing and rapid recovery for investors. Firstly There is hope that AI can solve the productivity problem. This of course presumes that the problem exists outside of an economics textbook, is soluble and that AI will deliver improvements without concomitant problems elsewhere. Every manager of every business or department on the planet seeks to increase productivity, albeit with more vigour in the private sector. While AI (the current deus ex machina for so many problems) might solve it, the solution could displace human white collar (clerical and low level managers) labour. How will those displaced workers find a new job? If they can’t, will the AI productivity increase be so good that an economy can afford to pay people to do nothing? It seems unlikely. Of course, this isn’t a problem for a global investor, who can move their money to where the growth is. It’s not the same for in the dole queue in Port Talbot.

The other possible amelioration is that “decarbonisation” yields lower cost energy, with a near zero marginal cost on additional usage, as well as an entirely new energy industry. The evidence is that this is baloney; intermittent renewables increase the cost of energy .The history of the idea of nuclear power being “too cheap to meter” is unfortunate; it is no truer of renewables now that it was of nuclear power in the 1950s.

Worse, the increasing usage of AI increases electricity demand rapidly and greatly. The United States is already concerned that it may not be able to power the anticipated growth in AI data centres, It’s not just generating the electricity, distributing it is also a problem. Fixing that costs serious money. For the UK alone the number is close to £3 trillion.

All of which means that a soft landing for the US (and thus the world) is unlikely. Toss in the increasing possibilities of war (and more tax to rebuild military capabilities) and the challenges the Houthis are presenting to trade through the Red Sea and the immediate future looks bleak. IT’s even bleaker if you believe Donald Trump to be the anti-Christ – he’s currently 10/11 on to be the next US President

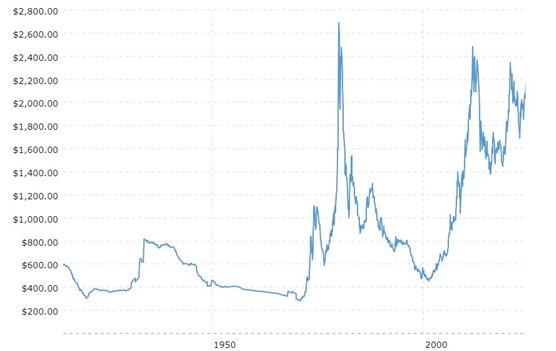

When things are bleak investors turn to gold (or Bitcoin for some) as a store of value. They may or may not be correct to do so, but the chart below confirms that is what they are doing. Note that this chart, courtesy of Macrotrends, is adjusted for inflation. The gold price is nearing an all-time high.

So much for the global view.

For the UK a US crash is usually very bad. The three ameliorations are worse. Printing more money will bring more inflation, rising interest rates and soaring bond yields. The 10% of government spending that services debt would rise. The wholesale adoption of AI might or might not increase productivity. It will definitely transfer funds from the UK to the “S&P magnificent seven” of Silicon Valley (Amazon, Apple, Alphabet, Meta, Microsoft, Tesla, and Nvidia). That’s money that won’t be taxed in the UK. And of course the decarbonisation lunacy of net zero will transfer money from UK households to the producers of uranium, steel, iron ore, copper and rare earth materials. What works for the global economy does not necessarily work for the UK.

The UK’s budget was all politics and spin. Few Tory MPs can believe that they'll survive the election and this was more about setting political traps for Starmer. The election will happen long before the impact of the Hunt masterplan will be felt in the real economy – which has big problems coming at it from outside of the Whitehall and Westminster bubble. Whether Reeves and Starmer will make things worse or better is an open question, at least it is intellectually. They have the same economic policies as the Tories, plus getting closer to the EU. They will

face the same reality. The UK is borrowing about £120 billion a year to pay debt interest of about £100 million a year which has driven tax to record levels. When GDP falls further, as is likely if NIESER’s speakers were correct, there won’t be the tax take to pay the bills.

That's called insolvency.